GST on combined travel packages

The new idea of businesses comes with more challenges, more complexity and opportunity. As per Heading 9985 of GST Tariff Act, 2017, the rate of GST would be 5% (2.5% CGST+2.5% SGST) provided following conditions are met,

- Input tax credit on services availed by the entity will not be available. However, Input Tax Credit on the services taken from other Tour Operator is allowed.

- The entity shall indicate in its invoice that the amount charged is gross amount and inclusive of charges of accommodation and transportation.

Therefore, if an entity offers a package to a customer for let’s say Rs. 1,05,000/- inclusive of everything, then the invoice shall be generated for Rs. 1,05,000/- (Rs. 5,000/- being CGST & SGST) and entity has to specifically mention in invoice that amount includes accommodation and transportation etc. No input tax credit on services like hotels, air tickets etc. will be available to the entity. However, Input Tax Credit may be taken on the tour operator services procured from another tour operator.

On the other hand, the entity may charge GST at the rate of 18% (9% CGST+9% SGST) on the total amount. In that case, the entity will be eligible to take all input tax credit like rent, professional fee, lease line, telephone etc. on the services that the entity acquired for providing the underlined services i.e. Tour Operating.

However, most of the input tax credit will not be available to the entity due to the nature and place of supply of those services which are taken by the entity. The main expenditure that entity will occur would be of Boarding & Lodging and Hotel booking. In case of Hotel booking, the place of supply would be the location where the hotel is situated and thus the hotel will charge CGST & SGST on the invoice. If the entity is not registered under GST in the state where the hotel is situated, the entity cannot take the input tax credit on that particular invoice. Same goes with flight tickets. The place of supply in case of air fare would be the place from where the flight embarks and in case the entity does not have registration under GST in the state from where such flight take-off, the entity cannot take input tax credit of that invoice too.

Let’s understand the situation with an example. Suppose a customer from Delhi approaches Tour Operator which is situated and registered in Bangalore for a complete package of 5D /6N tour to Kerala. The entity quotes Rs. 1,00,000 (Excluding GST) for the tour. The breakup of the charges is as follows,

| Air fare (Economy class) from Delhi to Kochi and return 47620GST charged by the Airlines@ 5% 2380 | 50,000 |

| Hotel Charges 26785GST charged by Hotel@ 12% 3215 | 30,000 |

| Other Charges 8475GST Charged @ 18% 1525 | 10,000 |

| Entity’s Fees | 10,000 |

| Total | 1,00,000 |

In this case, entity can opt either to pay 5% GST (IGST) on Rs. 1,00,000/- i.e. Rs. 5,000/- and avail no input tax credit or to pay 18% GST (IGST) and may avail input tax credit. But the entity is not eligible to take input tax credit on Air fare and Hotel charges as the place of supply, in case of Hotel, would be Kerala and in case of Air fare, it would be in Delhi. However, if the entity gets itself registered in Kerala and Delhi, then it is possible for the entity to take input tax credit for these services also but that seems quite unfeasible considering the compliance burden which will be increased for the entity.

Further, in this case the entity must raise an invoice indicating specifically that the amount charged is gross amount and inclusive of charges of accommodation and transportation.

Though, most of the companies do operate as Tour Operator services, the entity may either provide services as an agent and charge commission on its service and take reimbursement in actual for the expenses that entity incurred for providing such services. Generally, small business entity opts for this model as in this model, the entity must pay tax only on the commission that it charges and not whole amount which is not even its revenue.

The entity may also opt to provide the underlined services on commission basis. In that case, the service will be categorized as ‘Intermediary’ and services like Boarding & Lodging etc. will be taken by the entity on behalf of customer. The entity will act as ‘Pure Agent’ and take reimbursement on actual basis from the customer.

As per section 2(13) of IGST Act, 2017,

“Intermediary” means a broker, an agent or any other person, by whatever name called, who arranges or facilitates the supply of goods or services or both, or securities, between two or more persons, but does not include a person who supplies such goods or services or both or securities on his own account”

And as per the Explanation to Rule 33 of CGST Rules, 2017,

“Pure agent” means a person who—

- enters into a contractual agreement with the recipient of supply to act as his pure agent to incur expenditure or costs in the course of supply of goods or services or both;

- neither intends to hold nor holds any title to the goods or services or both so procured or supplied as pure agent of the recipient of supply;

- does not use for his own interest such goods or services so procured; and

- receives only the actual amount incurred to procure such goods or services in addition to the amount received for supply he provides on his own account.”

In this case, the entity has to enter into an agreement with the customer to act as his pure agent and authorize itself to incur the expenses for services like Hotel, Taxi etc. on behalf of customer. The entity, in this case, will charge its commission (whatever agreed) from the customer and will take reimbursement of the expenses on actual basis which it incurred on behalf of customer.

Let’s understand this with our previous example. In that case, if the entity enters into an agreement with the customer to act as pure agent, then the entity will charge GST at the rate of 18% on Rs. 10,000/- only i.e. Rs. 1,800/- and will take reimbursement of Rs. 90,000/- as actual expense incurred on behalf of the customer.

However, in this model, there are certain conditions which need to be complied with. As per Rule 33 of CGST Rules, 2017,

“Notwithstanding anything contained in the provisions of this Chapter, the expenditure or costs incurred by a supplier as a pure agent of the recipient of supply shall be excluded from the value of supply, if all the following conditions are satisfied, namely, —

- the supplier acts as a pure agent of the recipient of the supply, when he makes the payment to the third party on authorization by such recipient;

- the payment made by the pure agent on behalf of the recipient of supply has been separately indicated in the invoice issued by the pure agent to the recipient of service; and

- the supplies procured by the pure agent from the third party as a pure agent of the recipient of supply are in addition to the services he supplies on his own account”

Taking the previous example further, the entity has to raise an invoice for Rs. 10,000/- and add 18% GST thereupon and will indicate separately in the invoice for the payment made by the entity as pure agent on behalf of the customer.

In case the entity takes services of any other Tour Operator, let’s say for planning the itinerary for the customers for particular packages, the entity can take input tax credit regardless of his choice to act as Tour operator or Agent.

For better understanding, let’s continue with the example cited above. In that case, let’s say 25% is the fixed charges for the other Tour Operator which will come out to be Rs. 2,500/- (on Rs. 10,000/-). Now, the other Tour Operator shall charge GST at the rate of 5% (i.e. Rs. 125/-). In this case, the entity can take input tax credit of Rs. 125/- even if the entity has opted to pay tax at the rate of 5% on the total amount.

The GST shall be charged and paid at the time of payment or invoice whichever is earlier. Therefore, for the purpose of GST, the entity shall recognize its revenue on the payment basis.

However, if the entity opts to act as ‘Pure Agent’ the GST shall be charged when the final invoice is raised or the receipts of the commission whichever is earlier.

Tax Slabs on Flights & Trains

- Economy class: 5 %

- Business class: 12 %

- Non AC train tickets: Tax free

- AC train tickets: 5 %

Tax Slabs on Hotels

- Upto INR 1000/night: Nil

- From INR 1001 to INR 7500/night: 12%

- Above 7500/night: 18%

Who Can You Claim the GST from?

You can claim the GST from both, your service provider, as well as the supplier:

- Travel service provider: The ITC will be claimed on the convenience fee charged buy them.

- Supplier: Here, the ITC will be claimed on the tax charged by the hotel/flight.

Steps to Claim Input Tax Credit

The process to follow for claiming ITC is:

- Provide your correct details to the travel service provider + supplier. Any error in these details will result in loss of ITC.

- Obtain GST invoice from your supplier (hotel/flight). ITC on flights can be availed for any destination. However, for hotels, the company needs to be registered in the same state as the booked hotel.

For example, if your company has a Delhi GSTIN, and you have booked a hotel in Nagpur, you will not be able to claim ITC. To be able to do so, you need a Maharashtra/pan India GSTIN.

- The travel service provider + supplier will upload the respective GST amount on the government website by the 20th of subsequent month. This can be checked by the company on their portal.

- This amount gets credited to the company as ITC.

Details Required on Your GST Invoice:

- Registered Name of the Company

- Registered Address of the Company

- Company GSTIN

- PAN Number

GST on Transport of Passengers by Rail

GST on rail tickets (passenger transport) is applicable at the following rates*:

- 18% GST on AC and First Class train tickets

- Nil GST on sleeper and general class tickets

- Nil GST on metro tickets/tokens

*The above list is not exhaustive and subject to periodic change.

GST on Road Transport of Passengers

Passenger road transport services feature various GST rates depending upon the mode of transportation chosen. The following are the key GST rates that are applicable to GST on transport of passengers by road*:

- Nil GST on passengers travelling by road on public transport

- Nil GST on transport by road of passengers by metered taxi/auto rickshaw/e-rickshaw

- Nil GST on transport by non-A/C contract carriage/stagecoach

- 5% GST on transport by A/C contract carriage/stagecoach (no Input Tax Credit)

- 5% GST on transport by radio taxi and similar services

- 18% GST on rental services of road vehicles including cars, buses, coaches (with or without operator)

*The above list is not exhaustive and subject to periodic change.

GST on Transportation of Goods

The transportation of goods carried out by air, rail, road and inland waterways incurs GST on transport at an applicable rate starting from nil GST. The following are some of the key goods that are exempt from GST on transport*:

- Relief materials designated for victims of man-made/natural calamities, mishaps, accidents, etc.

- Pulses, milk, salt, flour, rice and other food grains

- Agricultural produce/products and organic manure

- Military/defense equipment being transported

- Newspapers/magazines registered with Registrar of Newspapers

- If the gross amount charged for goods transport is less than Rs. 1,500

Exemption or Nil GST on transport is also applicable in the following cases:

- Transport of personal use or household goods

- Transport of goods of unregistered persons

Apart from the above cases, GST on transport of goods by a GTA (goods transport agency) features the following taxation rates:

- 5% GST on transport in case ITC (input tax credit) is not availed

- 12% GST is applicable in case ITC is availed

Alternately, the following GST rate may also be applicable:

- 18% GST is applicable to rental services of road vehicles including trucks (with or without operator)

- 18% GST is applicable to rental services of freight aircraft (with/without operator)

- 18% GST applicable on rental services of water vessels including freight vessels (with/without operator)

What is a GTA?

As per the GST Act, a GTA or goods transportation agency refers to any person/entity that issues a “consignment note” or similar document and provides services such as transport of goods by road. As per the definition, a GTA might not always refer to an individual/business that is hiring out vehicles for transportation of goods. Thus it is individuals/businesses that issue a “consignment note” that qualify as GTA. Apart from transportation from consignor to consignee, other key services provided by a GTA include:

- Loading/unloading goods,

- Packing/unpacking goods,

- Trans-shipping i.e. shipping from one intermediary to another instead of end to end transport

- Temporary warehousing

Consignment Note and eWay Bill

Consignment note and eWay bill are two key documents involved in the transportation of goods. The consignment note is a document issued by a GTA (goods transportation agency) in lieu of a receipt of goods for transporting goods by road. Once a consignment note is issued, the lien of goods is transferred to the transporter i.e. the responsibility of goods remains with the transporter till the consignment is delivered to the consignee. No extra charges need to be paid for generating a consignment note which is generated by the transporter. However, the document will contain details of who is paying the GST on transportation and goods included in the consignment.

An eWay Bill is to be generated before goods are transported. This document has to be generated on the official eWay Bill Portal and is a key document for ensuring compliance with GST rules. The e-Way bill is a mandatory requirement for all GST registered individuals and businesses involved in the transport of goods by road from one location to another (whether within transportation occurs within the same state or interstate). Details included in the eway bill include GST paid on goods being transported, name of consignee and consignor as well as details of vehicle being used to transport the goods.

Hospitality and Tourism under the GST Regime

Under the Goods and Service Tax, the hospitality sector stands to reap the benefits of standardised and uniform tax rates, and easy and better utilization of input tax credit. As the final cost to the end user decreases, the industry attracts more overseas tourists than before.

This ideally results in improved revenues for the government, and there are many pros to this new tax regime which could help the industry’s growth in the long run. For instance, complementary food (like breakfast) was taxed separately under VAT, but now it will be taxed under GST as a bundled service. Let’s have a look at the rates for this industry in detail:

| GST Rates for Hotels based on Room Tariff (with effect from 1st October 2019) | |

| Tariff per Night | GST Rate |

| < Rs.1,000 | No Tax |

| Rs.1,001 -7,500 | 12% |

| = or > INR 7,501 | 18% |

| GST Rates applicable for Hotel Industry | |

| GST Rates for Hotels based on Room Tariff (Up to 30th September 2019) | |

| Tariff per Night | GST Rate |

| < Rs.1,000 | No Tax |

| Rs.1,000 -2,499.99 | 12% |

| Rs.2,500 -7,499.99 | 18% |

| = or > INR 7,500 | 28% |

| GST Rates applicable for Hotel Industry |

| Particulars | Amount | Amount |

| I) BASIC ROOM | Before GST | After GST |

| Room tariff | 2700 | 2700 |

| Luxury charge on Stay( 10% as per Maharashtra) | 270 | |

| Service Tax @ 9% | 243 | |

| GST @ 12% | 324 | |

| TOTAL BILL | 3213 | 3024 |

| II) ROOM WITH COMPLIMENTARY BREAKFAST | Before GST | After GST |

| Room tariff | 2200 | 2200 |

| Complimentary breakfast | 500 | 500 |

| Luxury charge on Stay( 10% as per Maharashtra) | 220 | |

| Service Tax @ 9% | 198 | |

| VAT @ 14.5% on food | 73 | |

| GST @ 12% | 324 | |

| TOTAL BILL | 3191 | 3024 |

| III) ROOM WITH COMPLIMENTARY BREAKFAST | Before GST | After GST |

| Room tariff | 8000 | 8000 |

| Complimentary breakfast | 2500 | 2500 |

| Luxury charge on Stay( 10% as per Maharashtra) | 800 | |

| Service Tax @ 9% | 720 | |

| VAT @ 14.5% on food | 363 | |

| GST @ 18% | 1890 | |

| TOTAL BILL | 12383 | 12390 |

| A break-up of the hotel prices pre and post GST implementation |

Hotel Room Rent

Changes proposed in 14th GST Council Meeting dated 18th& 19th May, 2017 effective from 01-07-2017

| Sl. No. | Room Rent | GST Rate |

| 1 | Rs. 0 to Rs. 1,000/- per day | Exempt |

| 2 | Rs. 1,001/- to Rs. 2,499/- per day | 12% with full ITC |

| 3 | Rs. 2,500/- to Rs, 4,999/- per day | 18% with full ITC |

| 4 | Rs. 5,000/- and above per day | 28% with full ITC |

Changes proposed in 37th GST Council Meeting dated 20-09-2019 effective from 01-10-2019

| Sl. No. | Room Rent | GST Rate |

| 1 | Rs. 0/- to Rs. 1,000/- per day | Exempt |

| 2 | Rs. 1,001/- to Rs. 7,500/- per day | 12% with full ITC |

| 3 | Rs. 7,501/- and above per day | 18% with full ITC |

Thus, the final rate structure for hotels applicable as on date may be summed up as follows:

| Sl. No. | Room Rent | GST Rate | Chapter/ Section/ Heading |

| 1 | Rs. 0/- to Rs. 1,000/- per day | Exempt | Heading 9963(Accommodation, food and beverage services) |

| 2 | Rs. 1,001/- to Rs. 7,500/- per day | 12% with full ITC | |

| 3 | Rs. 7,501/- and above per day | 18% with full ITC |

Restaurant Industry

Changes proposed in 14th GST Council Meeting dated 18th& 19th May, 2017 effective from 01-07-2017

| Sl. No. | Room Rent | GST Rate |

| 1 | Restaurants not having facility of air-conditioning or central heating at any time during the year and not having licence to serve liquor | 12% |

| 2 | Restaurants having facility of air-conditioning or central heating at any time during the year (whether serving liquor or not) | 18% |

| 3 | Restaurants serving liquor | 18% |

| 4 | Other than above | 18% |

Changes proposed in 23rd GST Council Meetings dated 10-11-2017 effective from 15-11-2017

| Sl. No. | Room Rent | GST Rate |

| 1 | All stand-alone restaurants irrespective of air conditioned or otherwise | 5% GST without ITC |

| 2 | Food parcels (or takeaways) | 5% GST without ITC |

| 3 | Restaurants in hotel premises having room tariff of less than Rs 7500 per unit per day | 5% GST without ITC |

| 4 | Restaurants in hotel premises having room tariff of Rs 7500 and above per unit per day (even for a single room) | 18% GST with full ITC |

| 5 | Outdoor catering | 18% GST with full ITC |

Changes proposed in 37th GST Council Meeting dated 20-09-2019 Effective from 01-10-2019

| Sl. No. | Room Rent | GST Rate |

| 1 | Outdoor catering services other than in premises having daily tariff of unit of accommodation of Rs 7501 | 5% GST without ITC |

| 2 | Catering in premises with daily tariff of unit of accommodation is Rs 7501 and above | 18% with ITC |

| 3 | Indian Railways Catering and Tourism Corporation Ltd. or their licensees/ Indian Railways | 5% GST without ITC |

Thus, the final rate structure for restaurants applicable as on date may be summed up as follows:

| Sl. No. | Room Rent | GST Rate | Chapter/ Section/ Heading |

| 1 | All stand-alone restaurants irrespective of air conditioned or otherwise | 5% GST without ITC | Heading 9963(Accommodation, food and beverage services) |

| 2 | Food parcels (or takeaways) | 5% GST without ITC | |

| 3 | Restaurants in hotel premises having room tariff of less than Rs 7500 per unit per day | 5% GST without ITC | |

| 4 | Restaurants in hotel premises having room tariff of Rs 7500 and above per unit per day (even for a single room) | 18% GST with full ITC | |

| 5 | Indian Railways Catering and Tourism Corporation Ltd. or their licensees / Indian Railways | 5% GST without ITC | |

| 5 | Outdoor catering services other than in premises having daily tariff of unit of accommodation of Rs 7501 | 5% GST without ITC | |

| 6 | Catering in premises with daily tariff of unit of accommodation is Rs 7501 and above | 18% with ITC |

E-Commerce Operators

E-Commerce Operators like Oyo Rooms, Swiggy, Zomato etc. have become an indispensable part of the hotel and restaurant industry. A major portion of the revenues of the industry is routed through these online platforms. These operators route orders to hotels and restaurants and in return they charge commission from them at agreed rates. The impact of such transactions may be understood as under:

- GST on hotel tariff or restaurant bills shall be charged as usual according to the prescribed rates which has been discussed above.

- GST on commission paid to E-Commerce Operators shall be 18%.

Let us understand the billing procedure followed by them:

Hotel Industry

| Sl. No. | Particulars | Amount (Rs.) |

| 1 | Room Tariff Charges | 10,000.00 |

| 2 | Discount 30% of 1 | 3,000.00 |

| 3 | Net Bill Value (1-2) | 7,000.00 |

| 4 | GST @ 12% on room tariff (5% of 3) | 840.00 |

| 5 | Total Payable by Customer (3+4) | 7,840.00 |

| 6 | Service Fee of E-Commerce Operator (40% of 3) | 2,800.00 |

| 7 | GST @ 18% on Service Fee (SAC 996813) [18% of 6] | 504.00 |

| 8 | Total Bill of E-Commerce Operator (6+7) | 3,304.00 |

| 9 | Net Payable to Hotel by E-Commerce Operator (5-8) | 4,536.00 |

Note:

- GST rate on hotel accommodation services is assumed to be 18% in above example, however it can also be 12% depending upon the room tariff in hotel.

- TCS Provisions on E-Commerce Operators have been ignored in above table.

- In the above, example the transaction value was less than Rs. 7,500/- and so 12% rate was charged and not 18%.

Restaurant Industry:

| Sl. No. | Particulars | Amount (Rs.) |

| 1 | Restaurant bill value | 100.00 |

| 2 | Restaurant Discount 10% | 10.00 |

| 3 | Net Bill Value (1-2) | 90.00 |

| 4 | GST @ 5% on food bill (3*5%) | 4.50 |

| 5 | Total Payable by Customer (3+4) | 94.50 |

| 6 | Service Fee of E-Commerce Operator | 10.00 |

| 7 | GST @ 18% on Service Fee (SAC 996813) [6*18%] | 1.80 |

| 8 | Total Bill of E-Commerce Operator (6+7) | 11.80 |

| 9 | Net Payable to Restaurant by E-Commerce Operator (5-8) | 82.70 |

Note:

- GST rate on restaurant services is assumed to be 5% in above example, however it can also be 18% depending upon the room tariff in hotel.

- TCS Provisions on E-Commerce Operators have been ignored in above table.

Applicability of Reverse Charge Mechanism

Reverse Charge Mechanism u/s 9(4) of the CGST Act, 2017 is not applicable to hotel and restaurant industry and thus no tax under the mechanism is to be paid.

Time of Supply

As per Section 13 of the CGST Act, 2017, time of supply in case of services shall be the earliest of the following:

- the date of issue of invoice by the supplier, if the invoice is issued within the period prescribed under sub-section (2) of section 31 or the date of receipt of payment, whichever is earlier; or

- the date of provision of service, if the invoice is not issued within the period prescribed under sub-section (2) of section 31 or the date of receipt of payment, whichever is earlier; or

- the date on which the recipient shows the receipt of services in his books of account, in a case where the provisions of clause (a) or clause (b) do not apply:

Thus, time of supply in case of hotel and restaurant services shall be:

If invoice generated,

- Time of issuance of invoice, or

- Time of provision of service Earlier

- Time of recording in books of accounts

If invoice not generated,

- Time of receipt of payment, or

- Time of provision of service Earlier

- Time of recording in books of accounts

Place of Supply

Section 10(3) of the IGST Act, 2017 states as follows:

“(3) The place of supply of services,

by way of lodging accommodation by a hotel, inn, guest house, home stay, club or campsite, by whatever name called, and including a house boat or any other vessel; or

(4) The place of supply of restaurant and catering services, personal grooming, fitness, beauty treatment, health service including cosmetic and plastic surgery shall be the location where the services are actually performed.”

From, the above, it is clear that place of supply in case of hotel industry shall be the place of location of immovable property and in case of restaurant services shall be the location where the services are actually performed. The above provision gives rise to certain issues which has been discussed below:

Supplier and Recipient in separate states

If the hotel is located in Guwahati and the recipient of service is located in Delhi. In this case, the place of supply of service shall be Guwahati and CGST and Assam GST (AGST) will be charged and not IGST. Further, the recipient of service will not be able to avail ITC of the tax paid on such transaction as GST paid in Assam is not eligible in Delhi GST.

Conclusion

The industry after much uncertainty has finally reached a stage where we can say that the stabilisation of rates has come. However, the Corona Pandemic has created havoc in the industry and if proper incentives are not accorded to the sector, it might witness a collapse and that will lead to a huge loss to the overall economy.

Impact of GST on Cab Services

Taxis are an important part of our lives. Especially for cities where other forms of transport are not very accessible, taxis form the lifeline of daily commuters. In fact, for the emerging white-collar or pink-collar segment of the society, taxis are godsent.

Many types of cabs are available in India. There are basic taxis which you can hail on the road (available in cities like Kolkata & Mumbai). Other cities (like Bangalore, Hyderabad) have only radio taxis like Ola, Uber, etc. Taxis aren’t just four-wheeled motorised vehicles.

You also have transportation like bullock carts, vegetable carts etc. that are considered similar to taxis in rural and semi-urban areas and who belong to the unorganised sector and never paid any taxes anyways However, the main impact of GST on cabs will be on the radio taxis, the taxis you hire through an app or phone.

What is a radio taxi?

GST clearly defines radio taxi as a taxi including a radio cab, by whatever name called, which is in two-way radio communication with a central control office and is enabled for tracking using Global Positioning System (GPS) or General Packet Radio Service (GPRS). This includes cab aggregators like Ola and Uber.

Service Tax

Service tax (with 60% abatement) was applicable on-

- A contact carriage (horse carriage)

- A radio taxi.

- “A stage carriage” – bus

It means service tax applied on radio taxis and AC buses but not on normal metered taxis like yellow taxis of Kolkata. Effective service tax was 6%.

Reverse Charge Mechanism

As per the reverse charge notification, radio taxi companies are liable to pay GST under reverse charge. Earlier rent-a-cab services had partial reverse charge mechanism. Service receivers (rent-a-cab services) were liable to pay 50% under RCM if the service providers (drivers) were not availing abatement. 50% was borne by the service provider. However, if Service provider is availing abatement then service receiver is liable to pay 100% of service tax payable on abated value. To remove such confusion and complications under GST, the entire onus is on the service receiver, i.e. Ola.

How will it work?

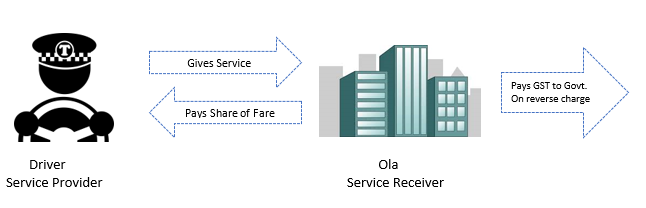

Ola Cabs sign up driver to ply passengers in cars. Drivers are providing chauffeur/driving services to Ola. Ola is the service receiver and pays drivers a share of the fare collected from passengers.

For example, a driver is to receive Rs. 100 as share of fare. Ola will pay Rs. 100 to the driver and deposit Rs. 5 to the government. On later providing the service to the passenger, Ola will collect GST on the fare. Ola pays GST on the drivers’ services on reverse charge basis. Ola can claim the ITC on tax paid under RCM and adjust with output taxes payable. The aim of reverse charge is to bring this unorganised sector under the tax umbrella. It also removes the burden of tax compliance from individuals with limited resources (drivers) to large companies (Ola) with enough resources.

GST Rate

There are two options with the service provider regarding GST Rate

Option – 1: Pay GST at a rate of 5%. In this option, the person is allowed to take input tax credit of only GST paid on cab services taken from other persons. Any other GST paid cannot be taken as input tax credit and will simply lapse.

Example – ABC Ltd, a cab service provider, enters into an agreement with XYL Ltd, a corporate entity. ABC Ltd. doesn’t have its own cars, so they take cars from MNR. In the given case MNR will charge GST at the rate of 5% from ABC Ltd. and ABC Ltd. will charge GST at the rate of 5% to XYL Ltd. and ABC Ltd. will take credit of GST paid to MNR because the service provider is in the same line of business but ABC Ltd. will not be able to take credit of GST paid on telephone bill.

Option – 2: Pay GST at the rate of 12%. In this option, the person is allowed to take input tax credit of all input goods and services subject to general restrictions on the use of input tax credit.

Example – In the example given above, ABC Ltd. can take credit of GST paid on telephone bill if they pay GST at the rate of 12% on outward supply of service.

There can be a case when the customer is charged based on fuel plus service charges. In that case, GST is to be charged at a rate of 18% on service charges. No GST is applicable on fuel part in that case.

Case In Which GST Is Payable On Reverse Charge By Service Receiver

A person who is not a body corporate and opted to pay GST at rate of 5% is not required to pay GST on providing services to a body corporate. Such body corporate has to pay GST on reverse charge basis on such services. (This rule is applicable from 1st October 2019)

For example: An individual is registered in GST and provides services to a private limited company. He is not required to charge GST in the invoice. He just charge amount for services and mention that “GST payable on Reverse charge basis” in the invoice.

Place Of Supply For Rent A Cab

Place of supply for services provided to a registered person is the place of such registered person, i.e. place of the recipient. For example – A cab service provider registered in Delhi gives service to a person registered in Rajasthan in the state of Gujarat. The place of supply in such case will be Rajasthan even when the service is provided in Gujarat.

If car rental services are provided to the unregistered person, then the place of supply will be the location where the passenger embarks on the conveyance for a continuous journey, i.e. the state/UT where the passenger starts his journey.

If the right to passage is given for future use and the starting point is not known at the time of issue of the right to passage, the place of supply of such service will be location of the recipient if the address is available on record. If such an address is not available, then the location of the service provider is place of supply.

| Location of Cab service provider | Registration status of service recipient | Location of Cab service receiver | Location Where journey starts | Place of supply for the agent | GST to be charged by the service provider |

| Gujarat | Registered | Gujarat | Rajasthan | Gujarat | CGST + SGST |

| Gujarat | Registered | Rajasthan | Gujarat | Rajasthan | IGST |

| Gujarat | Unregistered | Rajasthan | Rajasthan | Rajasthan | IGST |

| Gujarat | Unregistered | Not known | Rajasthan | Rajasthan | IGST |

| Gujarat | Unregistered | USA | Rajasthan | Rajasthan | IGST |

GST On Ola, Uber And Drivers Operating Through Them

GST is payable on cab services provided through Ola or uber.

Such service is covered under Section 9(5) of CGST Act. Section 9(5) states that the e-commerce operator (Ola, uber) is required to collect and pay GST to the government rather than the person who is providing cab service.

Therefore, cab drivers are not required to collect and pay GST.

Also, such drivers are not required to get registered even if the turnover is more than the specified limits. So, if a person is operating five cars through uber and has a turnover of Rs. 25 lakh then also he is not required to register. If a driver is registered then also he is not required to collect GST for service provides via Ola.

ITC by service receiver

GST paid on rent a cab service is specifically disallowed under Section 17(5) of CGST act. Therefore, such GST paid cannot be taken as input tax credit. However, if the service receiver is also cab services provider then he can take input credit of such GST.

Corporate Service By OLA And Uber

Ola & Uber also provide cab services to corporate entities. In this case, Cab aggregators take services from cab drivers and provide it to corporate.

Cab aggregators will give fees to cab drivers and later they will reimburse it from the corporate vide issuing debit note.

Further, cab aggregators will collect commission by issuing commission invoice to corporate for providing technology aggregation services to them.

Cab aggregator will charge GST at the rate of 5% on reimbursement debit note and 18% will be charged on commission invoice.

The corporate cannot take ITC of GST paid on reimbursement debit note but they can take credit of invoice issued for commission charges for the use of Technology aggregation services of cab aggregator.

Let us understand this with an example:

Ola, a cab aggregator, has entered into an agreement to provide service to reliance industries. Ola doesn’t have its own cabs; they use aggregation technology platform by which M/s. Akash cars is able to provide cab service to Reliance Industries on behalf of Ola. The transaction will be done as follows:

| Ola to M/s. Akash cars | Debit note by Ola to Reliance | Commission Invoice by Ola to Reliance |

| Trip charges 1,000 GST @ 5% 50 Total 1,050 Ola will pay 1,000 to M/s. Akash cars and pay GST to the government. | Trip charges 1000 GST @ 5% 50 Total 1,050 Ola will get reimbursement of charges from Reliance. No ITC will be available to Reliance. | Commission 200 GST @ 18% 36 Total 236 Ola will charge a commission from Reliance for using aggregation services of ola. Reliance can claim ITC of GST on the commission charged. |

Services By Tour Operators And Tour Agents

Tour operator may provide a bundle package to its customers. For example – A tour operator gives a package of Rs. 50,000 to a person which includes hotel, cab and entertainment park tickets. Now the question is which GST rate is to be applied.

There can be four situations in this case as below

- Tour operator sells a package and charges a flat fee – In this case, GST rate applicable on tour package will be applicable on total charges. For example – A tour operator gives a package of Rs. 20,000 which include hotel, cab etc. then GST rate applicable on tour package is chargeable on Rs. 20,000.

- Tour operators sell a package and charge separately for all services – In this case GST rate as applicable on services is applicable on individual services. For example – The tour operator charges Rs. 10,000 for hotels, Rs. 5,000 for cab and Rs. 3,000 for entertainment park tickets. The GST rate as applicable on the hotel is chargeable on Rs. 10,000, GST rate applicable on the cab is applicable on Rs. 3,000 and so on.

- Tour operator sells a package and acts as pure agent for some service – In this case, GST rate applicable as per point no. 1 and 2 above. And for service for which he is acting as pure agent will be shown as reimbursement. For example, a tour operator gives a package of Rs. 30K to a client. Tour operator doesn’t include cab service in this package. On demand by the client, he contacts a cab driver and driver told him charges or Rs. 8K. The tour operator charges this Rs. 8k from the client. In this case, he is acting as a pure agent and thus he need not charge GST on such Rs. 8k. Also, he is not entitled to Input tax credit for such service. There are certain conditions to be considered as a pure agent as below

- The payment made by the pure agent on behalf of the recipient of supply has been separately indicated in the invoice issued by the pure agent to the recipient of service.

- The supplies procured by the pure agent from the third party as a pure agent of the recipient of supply are in addition to the services he supplies on his own account.

- The person does not use for his own interest such goods or services so procured.

- He receives only the actual amount incurred to procure such goods or services in addition to the amount received for supply he provides on his own account.

- If the tour operator is giving tour package services on a commission basis to the passenger – Some tour operator books all services on behalf of passenger and charges commission for such services. GST will be leviable at the rate of 18% on such commission. Tour operator can take input tax credit for GST paid on cab services other than in case of a pure agent.

ITC On Car Purchased By Cab Owner

Input tax credit on cars purchased is specifically prohibited under section 17(5) of CGST Act. But it is available if the purchased car is used for taxable supply of transportation of passengers. Thus, ITC on car is available for cab owners in the month of purchase.

Also, note that persons opted to pay GST at rate of 5% cannot take such input. Only persons opted to pay GST at rate of 12% can take such input.

In case of service provided via Ola or Uber and car is purchased then taking ITC on car is not possible as the driver is not required to pay GST as discussed earlier.

GST On Lease Paid By The Driver

Ola & Uber, cab aggregators are providing leasing of car services to its drivers. Cab aggregator buys a car and gives it to the driver on lease to use it for transportation of passengers on Ola & Uber app.

The driver will pay minimum initial deposits and daily/monthly rent to the cab aggregators. This leasing program is covered under GST. Therefore, such GST is payable on such lease amount.

For example, Ola will buy a car and pay GST on that car. Ola gives it to the driver on lease. Ola will collect daily/monthly rent with GST from drivers. Ola will get the ITC of GST paid on a car purchased as it is used for transportation of passengers.

GST Registration for Transport Service Providers

Majority of the businesses involved in providing passenger transport services would need to obtain GST registration and file GST returns as their annual aggregate sale turnover would be more than Rs.20 lakhs, or they would be involved in the providing of inter-state supply of services.

SAC Code for Passenger Transport Services

GST Rates in India are linked to SAC code or Service Accounting Code, a system of classification developed by the Service Tax Department in India for the levy of service tax. Under the SAC Code, passenger transport services fall under two groups, group 99641 for local transport and sightseeing transportation services of passengers and group 99642 long-distance transport services of passengers.

Goods, on the other hand, are classified using the HSN Code, an internationally accepted methodology for classifying goods in the course of import or export by over 200 countries.